Editor’s Note: This article is a follow-up to The Tax Cuts and Jobs Act – How Will It Affect YOU? published in the Winter 2018 issue.

On Aug. 8, the IRS issued proposed regulations for the newly created Section 199A 20 Percent Qualified Business Income (QBI) deduction. 199A has been one of the most talked about aspects of the Tax Cuts and Jobs Act since its passage last December. This provision of the act was included in the tax reform bill in an attempt to give pass-through entities (such as partnerships, LLCs and S corporations) and sole proprietorships similar tax savings that were provided to C Corporations (C Corp tax rates were reduced from a high of 35 percent to a flat 21 percent). The new 20 percent QBI deduction is effective for the 2018 tax year through 2025.

Although the new tax deduction is generous, the structure of the deduction is complicated with many limits, phase-ins, and phase-outs. Whether or not you will be able to take the deduction depends upon many factors, the key being your personal taxable income. Other factors include wages paid by the practice, the value of business property, nature of income, etc.

Physicians are especially impacted by limits on the deduction since the income is earned from what the law labels as a “Specified Service Trade or Business” (SSTB).

What is a Specified Service Trade or Business (SSTB)?

Most unincorporated business owners, partners and S Corporation shareholders benefit from the 199A deduction. However, Congress precludes some higher-income business owners from taking the deduction if the income is earned from an SSTB.

An SSTB is a trade or business involving the performance of services in the fields of health, law, accounting, actuarial science, performing arts, consulting, athletics, financial services, investing and investment management, trading, dealing in certain assets or any trade or business where the principal asset is the reputation or skill of one or more of its employees. Per IRS regulations:

The term “performance of services in the field of health” means the provision of medical services by physicians, pharmacists, nurses, dentists, veterinarians, physical therapists, psychologists and other similar health care professionals who provide medical services directly to a patient. The performance of services in the field of health does not include the provision of services not directly related to a medical field, even though the services may purportedly relate to the health of the service recipient. For example, the performance of services in the field of health does not include the operation of health clubs or health spas that provide physical exercise or conditioning to their customers, payment processing, or research, testing and manufacture and/or sales of pharmaceuticals or medical devices.

Based on this definition, physician practices are considered SSTBs, and therefore, limits apply on the available deduction.

How does the deduction work?

The QBI deduction is based off “pass-through income,” income reported on a Schedule K-1 earned from partnerships, LLCs and S Corporations or if a sole proprietor, what is reported on Schedule C of Form 1040 individual income tax return. Wages reported on a W2 or guaranteed payments paid to partners do not qualify as QBI. It excludes any investment-related items, such as interest, dividends or capital gains or losses from the sale of property. The maximum deduction available is 20 percent of QBI.

Although the deduction is calculated based on income earned from a trade or business (i.e. – the physician practice), the actual amount of the deduction is dependent on the taxable income of the individual. Most physicians with taxable income over $415,000 filing a joint return will be hard-pressed to qualify for the deduction. As such, it is possible for a large group practice to have some physicians qualify for a QBI deduction and some not qualify when there is a large variation in income among the owners.

The deduction itself is claimed on Form 1040 individual income tax return. Form 1040 will include a new line for the deduction in arriving at taxable income.

How do I know if I qualify to take the deduction?

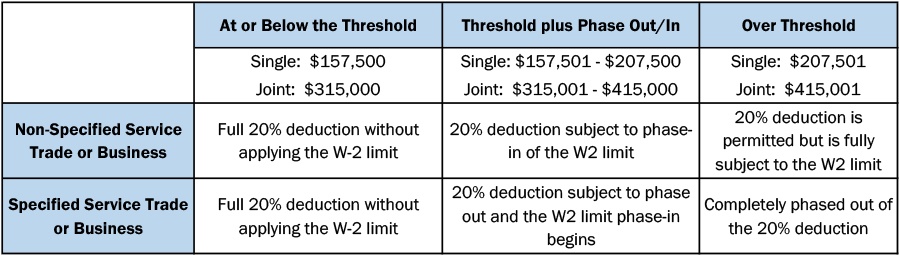

The deduction is fairly simple and straightforward for individuals with married filing joint taxable income of $315,000 or less ($157,500 or less if filing single). Those taxpayers receive the full 20 percent QBI deduction. Above those taxable income amounts, the 20 percent QBI deduction becomes subject to a tangled web of limitations, phase-ins, and phase-outs. Individuals with income from SSTBs (i.e. physician practices) are subject to even more limitations that, depending on the individual’s taxable income, quickly eliminate the 20 percent deduction altogether.

Let’s first examine the limits applicable to both service and non-service businesses alike once taxable income exceeds the limits noted above. The 20 percent qualified business income deduction is limited by the greater of:

- 50 percent of W2 wages paid by the qualifying business or

- 25 percent of W2 wages paid plus 2.5 percent of unadjusted basis of all qualified property.

These limits are phased in for joint filers with taxable income greater than $315,000 but less than $415,000 ($157,500 / $207,500 for non-joint filers) and result in a reduced 1991A QBI deduction.

In addition to the above limits, the ability to take the 199A QBI deduction for individuals with pass-through income from a SSTB is completely lost once individual taxable income exceeds $207,500 if filing single or $415,000 if filing joint. Phase out begins at $157,500 filing single and $315,000 filing joint.

The chart at the bottom of this section summarizes the various limitations, phase-ins and phase-outs for both SSTBs and non-SSTBs.

To illustrate, assume Dr. A is a sole practitioner who files a joint return. Her practice is organized as a single-member LLC. The qualified business income as reported on Schedule C of Dr. A’s 1040 is $240,000 after wages paid to staff of $195,000. Dr. A and her husband’s taxable income for the year is $295,000.

In this example, Dr. A’s tentative 20 percent deduction is $48,000 ($240,000 QBI* 20 percent). Since Dr. A’s overall taxable income is less than $315,000, she is able to take the full deduction of $48,000 since neither the W2 phase-in limit nor the SSTB phase-out limit applies.

But what if Dr. A’s taxable income is over the $415,000 limit noted above? Since the medical practice is considered a SSTB and income is over the allowed threshold, Dr. A is not allowed to take any amount as a QBI deduction.

It is important to note 199A generally requires taxpayers to identify QBI on a business-by-business basis. Physicians who own interests in other non-SSTB pass-through entities may still qualify for a 199A deduction for that trade or business.

IRS Anti-Abuse Regulations

Various planning strategies have been considered by physicians and their advisors on how to avoid the SSTB limitation. Some of these strategies became known as “crack and pack,” which involved splitting a practice into separate legal entities to isolate non-medical activities to qualify for some amount of deduction. One of the entities would provide the medical services and the other entity would lease office space, provide billing services, or various other administrative functions.

However, the regulations issued by the IRS contain various anti-abuse provisions – one of which significantly limits the ability to segregate activities among various entities when there is common ownership among the entities solely to qualify for the 199A QBI deduction. The proposed regulations state if any trade or business provides 80 percent or more of its property or services to an SSTB, and if that other trade or business and the SSTB share 50 percent or more common ownership, then that other business is considered an SSTB too. For purposes of this anti-abuse rule, ownership is both direct and indirect ownership by related parties.

It is a common practice for various components of a physician practice to be held in separate entities, often for legal protection and tax planning. One such example is real-estate held in a separate entity and rented to the practice. This is still acceptable; the anti-abuse regulations just prohibit taking a 199A QBI deduction in such circumstances.

The regs contain various other anti-abuse provisions, such as treating non-SSTB’s as an SSTB if they share expenses/overhead with a 50 percent commonly owned SSTB. In addition, there will be increased scrutiny over changes in classification between employee versus independent contractor or partner/shareholder status due to the impact on qualifying for the 199A QBI deductions. Physicians should consult with their attorney/tax advisor prior to making any such changes in an attempt to take a 199A QBI deduction.

Planning Opportunities

Although not every physician will be able to take advantage of the new 20 percent QBI deduction, the Tax Reform and Jobs Act still provides numerous other tax breaks, such as an overall reduction in individual income tax rates, elimination of some itemized deduction limitations, increased depreciation deductions, etc. For those physicians under the SSTB thresholds noted above, now is the time to time to consult with your tax advisor to ensure optimization of the 199A QBI deduction.

- Physicians under the SSTB threshold should review and evaluate the following items and discuss with their tax advisor and attorney:

- Whether he or she is operating the practice in the most appropriate entity form to qualify/maximize the 20 percent QBI deduction.

- Partners in a partnership currently receiving guaranteed payments should consider revising their partnership agreements and taking draws instead to increase QBI and the corresponding 20 percent deduction.

- For S Corporations, review compensation agreements and ensure a reasonable compensation is paid for services provided (not QBI), and pay the remainder of income as a distribution (does qualify for QBI).

In Summary

This summary merely scratches the surface of the 199A 20 percent QBI deduction and was written in the context of physician practices. Although the regulations are still in proposed form and not expected to be finalized until later this year, the Department of the Treasury has provided sufficient insight and interpretation of the law to plan for its implementation.

Executive Summary

- The new 20 percent QBI deduction is based on pass-through income earned from partnerships, S-Corps, LLC’s or sole proprietorships.

- W2 wages/guaranteed payments do not qualify as QBI.

- Deduction will be claimed on Form 1040 individual tax return.

- Claiming the deduction will be difficult, if not impossible to claim for physicians with taxable income over $207,500 if filing single or $415,000 if married filing joint unless there are sources of income from other non-SSTB pass-through entities.

- Newly issued IRS anti-abuse regulations limit the ability to split apart practice into various entities to isolate non-medical activities in order to take the deduction.

- Physicians earning under the above thresholds should meet with their tax advisor and attorney now to maximize potential deductions for 2018.

Mark Baker is a Principal with Jackson Thornton CPA’s and Consultants in Montgomery, Ala. He may be reached by calling (334) 834-7660 or email Mark.Baker@JacksonThornton.com. Jackson Thornton is an official partner with the Medical Association.